|

|

|

|

|

|

|

|

VIDEO: Dan discusses the current economic issues affecting the stock market.

|

|

|

One of the funny things about the stock market is that every time one person buys, another sells,

and both think they are astute.

William Feather

|

|

|

DAN'S BLOG

Thank-you!

Just a note for all the calls and emails I have received from many of you. I had a friend come up to me at a Celebration of Life for a mutual friend and give me a hug and he said “Thank you!” and I said “For what?” He said: “I read your blog and went to cash!”

It is nice to know that those in cash at the moment are enjoying the summer and not bothered by the market volatility and potential downside.

It is nice to know that those in cash at the moment are enjoying the summer and not bothered by the market volatility and potential downside.

The TSX is off -5.61% as of Monday’s close but last week at the end of Monday it was down -11% since we reallocated to cash on July 6.

As I have explained we expect things to be choppy but these big down days have not been our big concern. The real damage I believe will happen between September 10th and October 30th.

By the time our next Newsletter comes out at the beginning of October we will see if our concerns have come true?

Dan Loney

For more information on how Loney Financial can help, contact us at 604.534.6003 or Email: dan@loneyfinancial.com

|

|

More than half of Canadian students turn to ‘Bank of Mom and Dad’ before school year ends: CIBC

If past practice is any indication, the majority of post-secondary school students will likely run out of money before the school year ends — and end up turning to the Bank of Mom and Dad for help.

A new poll from CIBC has found that 51 per cent of post-secondary students tapped their parents for additional financial support last year because they ran out of money.

And according to the bank, there wasn’t much difference between students from higher- and lower-income families.

CIBC said some 48 per cent of students from families with household incomes of more than $125,000 tapped their parents for extra cash, compared with 52 per cent from families with household incomes of less than $75,000. CIBC said some 48 per cent of students from families with household incomes of more than $125,000 tapped their parents for extra cash, compared with 52 per cent from families with household incomes of less than $75,000.

Sarah Widmeyer, managing director and head of Wealth Advisory Services, at the bank, said that even though 86 per cent of parents surveyed considered themselves good role models for financial planning, some students were treating their parents like personal ATMs.

Widmeyer said young people need to understand that their parents may not always be willing or able to dispense extra cash and that being taught basic financial and budgeting skills before they go off to college or university is essential.

“Clearly, being a good financial role model doesn’t mean your children will understand how to manage their own finances,” she said.

“That’s why it is so important to teach them the importance of balancing a budget in their early teens because it’s a much a tougher lesson to learn when they are off living on their own for the first time in their lives.”

http://business.financialpost.com/personal-finance/young-money/more-than-half-of-canadian-students-turn-to-bank-of-mom-and-dad-before-school-year-ends-cibc

|

|

|

Mint.com is a fantastic tool. It is what I use to track my monthly budget for fixed and variable expenses. It will even track your discretionary spending if you want but most of the time my discretionary expenses (coffees, movies, eating out) are paid with cash. Check out this free service and if you use it you will be very impressed.

https://www.mint.com/

|

|

|

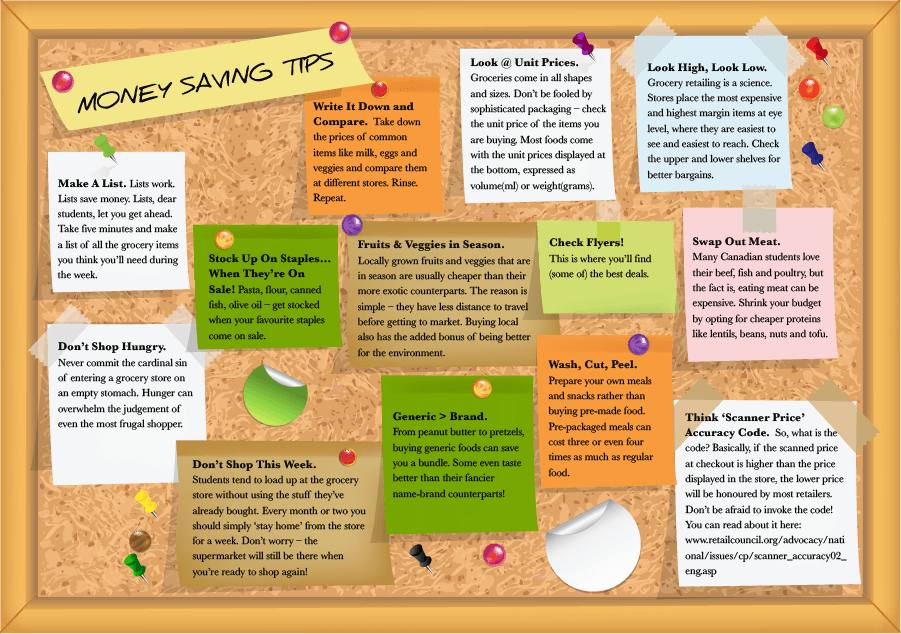

Back to School Money Saving Guide For Students

At LowestRates.ca, we know school is expensive. That’s why every September we release our annual Student Money Saving Guide to help students keep their finances -- and their futures -- looking good.

From tracking expenses to choosing a cellphone plan to picking the best financial apps, our guide offers tips and tools that, taken together, help save students thousands of dollars over the course of a single school year.

This year’s updated guide is divided into six parts:

- scholarships and bursaries,

- housing,

- transportation,

- food,

- budgeting

- day-to-day spending.

In 2015 we’re also including 10 featured schools where we breakdown and compare the costs associated with attending each institution. Our featured schools span from coast to coast and include Dalhousie University, McGill University, Queen’s University, Humber College, the University of Toronto, York University, the University of Western Ontario, Southern Alberta Institute of Technology, University of Calgary, and the University of British Columbia.

Read on to start your crash course in Money Management 101!

|

|

|

Cost of Waiting to Invest in Education Fund

|

|

|

Start Education Planning Now

Today’s children will need higher levels of training and education to secure employment in a world that is becoming increasingly competitive and technology driven. Obtaining a post-secondary education to meet these demands is also becoming more expensive as governments continue to cut spending to reduce deficits and balance budgets.

The current cost for four years of university education is approximately $60,000. This includes tuition rent, food, books and additional fees. In eighteen years, the total cost of a four-year university education will be $105,000, assuming costs increase by 3% per year.

Start Saving Now

The earlier you start saving, the larger your education savings nest egg will be thanks to the magic of compounding. But delaying even a year or two can affect the total amount you can save. Learn more about the why saving early can make a significant difference.

http://www.lifestylecalculators.com/the-cost-of-delaying-education-funding/

|

|

|

Are you ready for Manulife One?

|

|

Discover why the Clarkes have been recommending Manulife One and how it made their life easier.

http://www.manulifeone.ca

|

|

No more pencils, no more books — for recent graduates Fall is all about paying off debts.

Tyler Welch was a voice of fiscal prudence, preaching over the airwaves about budgeting and living within one’s means. His show was called Common Cents.

Once a week over the 2014-15 school year, Welch used his weekly slot on McMaster University’s campus radio station to dole out personal finance tips and tricks he thought his peers should know. He had just finished his undergraduate degree via correspondence, leaving the London School of Economics with a BA in international relations — and $24,245 in debt.

That is right around the Canadian national average, and with post-secondary classes reconvening next month, it is a figure many new and future graduates will soon confront.

“Just because you’re about to graduate doesn’t mean you’re a big shot, because you still have a bunch of money in debt,” Welch says. “But that’s what a lot of people fall into. They graduate, get their first high-paying job, and they’ve never seen a paycheque like that before. You squander it, and that’s how you end up in debt for 10 years.” “Just because you’re about to graduate doesn’t mean you’re a big shot, because you still have a bunch of money in debt,” Welch says. “But that’s what a lot of people fall into. They graduate, get their first high-paying job, and they’ve never seen a paycheque like that before. You squander it, and that’s how you end up in debt for 10 years.”

Welch plans to be debt-free by next February, less than two years after earning his diploma.

“I’ve been working like an adult, but living like a student,” says Welch, who has been employed full-time since graduating — first at the radio station, and now for an entrepreneurship program at McMaster.

“I still live in a house that I share with six other men, most of which are students. It’s dingy, but the rent is low. I bike everywhere, don’t own a car, try to not eat out too often and save close to 70 per cent of my income.”

For many Canadian students, money is an acute concern. The cost of an education mounts quickly, and post-tuition costs like textbooks, living expenses and ancillary course fees can add up to more than they — or their parents — anticipate. For many Canadian students, money is an acute concern. The cost of an education mounts quickly, and post-tuition costs like textbooks, living expenses and ancillary course fees can add up to more than they — or their parents — anticipate.

Students cover their expenses in many ways, including RESPs, student lines of credit and government loans. In B.C., Saskatchewan, Ontario, New Brunswick and Newfoundland and Labrador, prospective and current students can apply for “integrated” loans — combined assistance from the province and the federal government — which offer a six-month grace period after graduation before payments are due. But on the federal portion of the loan, usually about 60 per cent, interest accrues immediately.

In 2010, Statistics Canada found that half of university graduates left school indebted to either the government or another institution, and 41 per cent owed $25,000 or more. The mean undergraduate debt load that year was $26,300. When StatsCan followed up three years later, 34 per cent of the graduates with debt had paid it all off, and those with outstanding payments still owed, on average, $19,800.

Last week, a CIBC poll found that 37 per cent of current post-secondary students were unsure they’d be able to manage their finances after graduating, and 36 per cent anticipated a debt load of $25,000 or higher. “For a lot of (students), the financial literacy skills that they’re developing are still in their infancy. It’s difficult for them to manage this growing debt,” said Spencer Nestico-Semianiw, president of the Ontario Undergraduate Student Alliance and the McMaster Students Union’s vice-president of education.

It is a concern echoed by Patricia White, the executive director of Credit Counselling Canada. She says she often hears stories of new graduates taken aback by the debt they accumulated and unaware of how, or even to what institution, to make payments. It is a concern echoed by Patricia White, the executive director of Credit Counselling Canada. She says she often hears stories of new graduates taken aback by the debt they accumulated and unaware of how, or even to what institution, to make payments.

“It takes some concerted effort to really buckle down and control your expenses — even when you get a job right out of school. Even with the best of circumstances,” White says.

“That’s what we see: you’re not realistic about where things are at, and you need to be.

“You need to be paying that debt as soon as you can,” she says. “Other life experiences (are) coming down the road at you, whether it’s a wedding or a car or other future goals.”

Debt is a given for many students. But there are ways to keep it under control, White says, and it starts with sound money management.

She recommends establishing a spending plan and tracking purchases by sub-category — entertainment, food and drugstore goods, for instance, rather than just “miscellaneous” — so students have a better sense of where money can be saved and put towards debt. Any student loan repayment program should also account for other types of debt that will need to be paid for, like credit card bills or large investments, she adds.

“(Students) might be thinking of other debt — let’s say, for example, buying a used car, or something like that, to get to a job,” White says. “There’s a lot of things that need to be considered.”

But finding work can be a slow process.

Aliçia Raimundo was unemployed for six months after graduating from the University of Waterloo’s psychology and business program in 2012. Now, she holds three part-time positions, scratching out the equivalent of a 40-hour workweek. Aliçia Raimundo was unemployed for six months after graduating from the University of Waterloo’s psychology and business program in 2012. Now, she holds three part-time positions, scratching out the equivalent of a 40-hour workweek.

“It was a bit of a rude awakening, and especially with the economy the way it is, just the struggle to find a (sustainable) job that gives you enough to live on and pay off your debt,” Raimundo says.

Raimundo says she has erased her $15,000 debt load with the help of her parents — but added that many people are left to tackle their loans alone.

“There’s a lot of things compounded: inability to find a job, but also kind of not having money management, to know to pay it off right away,” she says.

Welch, meanwhile, is enrolled in a graduate correspondence program through the University of London, while working full-time in Hamilton. He turned down a chance to study international relations at the University of Edinburgh, which would have cost nearly $30,000 in tuition alone.

“The lifestyle I live has been exactly the same as it (was) when OSAP (the Ontario Student Assistance Program) was paying my bills,” he says. “It’s just now, I happen to have a bunch of extra income as well. I just didn’t change my lifestyle, but put all the extra money to debt, instead.”

http://business.financialpost.com/personal-finance/young-money/no-more-pencils-no-more-books-for-recent-graduates-fall-is-all-about-paying-off-debts

|

|

|

Five things to know about student debt

- Borrowing is not the only way. Some students qualify for federal and provincial grants, which do not need to be repaid. Canada Student Grants offers $250 a month for students from low-income families, plus stipends for those with disabilities or children.

- Beware the grace period. Students with “integrated” federal-provincial loans have six months after their last day of study before they must start paying. Interest on the federal share of the loan, though, kicks in right away.

- Payment varies by province. While integrated loans are repaid through the National Student Loans Service Centre, loanees in Alberta, Manitoba, Nova Scotia and P.E.I. make two separate payments: to the NSLSC and to their provincial service. Students in Quebec, meanwhile, only receive loans from the province.

- The alleviation option. Graduates with federal loans can apply for repayment assistance through the NSLSC. If approved, their province and the Canadian government will cover whatever interest is excused from the revised payment plan.

- Change the pace. To erase their loan more quickly or reduce long-term interest, former students can increase their monthly payments or make a bulk payment whenever they choose. Alternatively, people struggling to pay can apply to prolong the terms of their loan, resulting in a smaller monthly fee.

|

|

WHAT'S DAN READING?

Leading Me: Eight Practices for a Christian Leader's Most Important Assignment

by Steve A Brown

For many years I have had a real interest in leadership. What makes a great leader? For many years I have had a real interest in leadership. What makes a great leader?

This quest lead me to complete my Certificate in Advanced Leadership Development through Arrow Leadership.

This is a 24 month process which basically is like a faith based MBA focusing on leading organizations.

Dr. Steve Brown is the president of Arrow and I remember his teaching extremely well. His basic premise is that you cannot lead an organization until you first have done a good job of leading yourself.

Dr Brown addresses the need to understand your personal vision, unhook the bungee cords in your life, managing your time and leveraging your impact as a leader. The book is a pleasant read with many real nuggets of wisdom.

Dan

Purchase this book at Amazon.ca online.

|

|

|

Click here to see the story of a 35 year dream come true and learn about Loney Financial’s support of rescuing homeless children in Guatemala. Thank you to all the clients and associates that have helped to make this a reality.

|

|

|

COOKING WITH DENISE

Denise Bailey our Client Services Coordinator brings you a delicious monthly recipe from her renowned portfolio.

ONE POT CHILI MAC AND CHEESE

Prep Time: 10 minutes

Cook Time: 20 minutes

Total Time: 30 minutes

Serves 4

I have made this recipe several times now and it is quick, easy and, in my opinion, delicious!

I change up the type of beans that I use and usually make this for Saturday or Sunday lunch so there are leftovers!)

Enjoy!!!

Denise.  Ingredients:

Ingredients:

- 1 tablespoon olive oil

- 2 cloves garlic, minced

- 1 onion, diced

- 8 ounces ground beef

- 4 cups chicken broth

- 1 (14.5-ounce) can diced tomatoes

- 3/4 cup canned white kidney beans, drained and rinsed

- 3/4 cup canned kidney beans, drained and rinsed

- 2 teaspoons chili powder

- 1 1/2 teaspoon cumin

- Kosher salt and freshly ground black pepper, to taste

- 10 ounces uncooked elbows pasta

- 3/4 cup shredded cheddar cheese

- 2 tablespoons chopped fresh parsley leaves

Directions:

Heat olive oil in a large skillet or Dutch oven over medium high heat. Add garlic, onion and ground beef, and cook until browned, about 3-5 minutes, making sure to crumble the beef as it cooks; drain excess fat.

Stir in chicken broth, tomatoes, beans, chili powder and cumin; season with salt and pepper, to taste. Bring to a simmer and stir in pasta. Bring to a boil; cover, reduce heat and simmer until pasta is cooked through, about 13-15 minutes.

Remove from heat. Top with cheese and cover until melted, about 2 minutes.

Serve immediately, garnished with parsley, if desired.

|

|

|

|

|

Solutions Magazine

PREPARE FOR TOMORROW, TODAY - Taking control of your future starts with a plan.

Read More (PDF) >

|

|

|

|

Articles

A Guide to Not Retiring

Some people nearing retirement age simply don’t want to leave their jobs. But defying expectations can be difficult—in the office and at home.

It’s an inescapable reality of getting older: At some point, everybody expects you to retire. There’s your spouse, who perhaps is already retired and is looking forward to enjoying a relaxing life with you —

Read More >

|

|

|

|

|

|

|

|

|

|