Like driving with a foot on the gas pedal and the handbrake on.Your Bi-weekly update on edible oils & fats by Aveno May 25th, 2020

Low petroleum prices and lower demand caused by lockdowns continue to affect prices of many goods. But, a number of factors popping up, may gradually have a stabilizing effect on price levels.

Begin May the EU Commission published measures to support the EU food and agricultural sectors. These measures enable some sectors to help re-balance supply to adjust to the shifting demand caused by the COVID-19 crisis. They include private storage aid (e.g. for butter), flexibility in the implementation of market support programs (e.g. for wine and olive oil) and others.

In China, slowly breaking out of its lockdown, consumption is picking up and warehouses need to be refilled. This may stimulate demand on the global markets for oils, meals and oilseeds and lead to a gradual recovery in price levels. Similar effects are expected from India and we already saw Indian palm and soy oil purchases picking up.

But often good news is counterbalanced by bad news like the threat of a “cold war between the U.S. and China”. Or till a cure or vaccine is found we face the risk of a second wave of infections.

Everyone is set to go but it’s like driving with a foot on the gas pedal and the handbrake on.

General situation in the oils and fats complex Markets are trying to assess how much demand destruction has to be priced in for forward months. In China consumption is picking up while it is declining in the rest of the world. Global reduction of consumption this year is a fact. Global biodiesel production is expected to drop 5 million tons but also the food sector is experiencing lower demand. Palm oil (popular frying and cooking oil in restaurants) demand will mostly suffer in most countries, soy oil in the U.S. and rapeseed oil in EU.

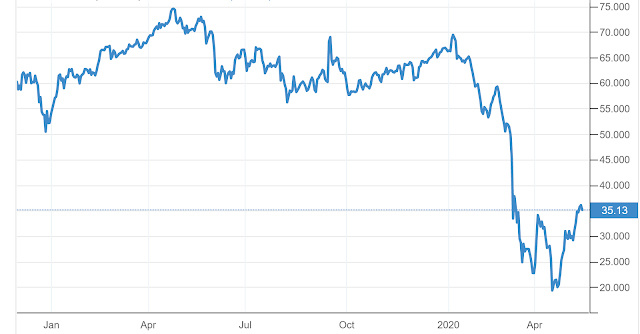

Data Source: Thomson Reuters

Rapeseed oil Harvest expectations in EU were revised downwards again due to dry weather in Germany, France and Poland. The start of the 20/21 marketing year will be one with prospects of tight supplies. Rapeseed oil continues to trade at a significant premium over soybean and palm oils. China is buying and there are renewed flows of Canadian canola products to China.

Palm oil Weakening demand as a result of the pandemic. Increasing stocks in producing countries (Indonesia, Malaysia) are expected to impact producer margins, which in the long run might lead to lower production. But palm trees produce continuously year-round with a production peak usually seen in Sept/Oct/Nov. And after the Ramadan, traditionally production picks up.

The implementation of the B20 biodiesel program (blend of 20 per cent palm methyl esters and 80 per cent petroleum diesel) in Malaysia’s transportation sector is postponed: in Sarawak to Sept 1st, 2020, instead of April 2020, and in Sabah to Jan 1st instead of August 2020. The program, a government initiative, is expected to absorb 534,000 MT of palm oil per year.

Also, Indonesia is studying how it can continue to support its biodiesel industry in the face of reduced fuel demand. With B30 already in place and plans for B40 before the end of 2022, low petroleum prices weigh heavily on the country’s capacity to continue with the plans.

The pandemic is expected to impact palm oil production, but it is not yet clear by how much and if lower blending will offset that lower production.

Soybean oil Soybean oil is still cheap and demand from the energy sector is low. The Argentinean soybeans crop is estimated at around 50 million tons (down 4 vs previous year), the Brazilian crop at 123 million tons (up 2 vs last year). China is shipping beans from South America.

Sunflower oil The premium over soybean and palm oil continues to hold. Next crop looks bigger than last crop with the expansion of cultivation areas in the Black Sea region. Dry weather may still impact negatively the yields. Old crop is more expensive than new crop, as Turkey and other countries have depleted sun seed/oil stocks with large purchases.

Animal fat The meat sector faces a lot of headwinds. In Ireland, some slaughterhouses closed in recent weeks because of falling meat demand and because of Covid-19 infections in the workplace. Similar problems were observed in Germany, France, The Netherlands and probably elsewhere in EU. In either case if plants continue to operate, social distancing also reduces slaughter capacity.

Containment measures across Europe are leading to a major slowdown in slaughter activities. The beef market is affected but more or less same goes for other species. April witnessed a decline of around 13% in the slaughter of cattle and up to 33% in the slaughter of calves due to lost demand from restaurants and a drop in the supply to consumers in their usual purchasing channels. This impacts the animal fat market which, despite a sharp drop in other oils & fats prices, is resisting because of the significant drop in available quantities of fat. Most players don’t know if and how much material will be available in the coming weeks and months. Something will have to break.

Laurics Both palm kernel and coconut oil production are seen declining in coming months.

Palm kernel oil stocks have been heavy and PKO lost demand in oleochemical, animal feed and food markets but demand from soap and healthcare producers remains strong. Coconut oil is still 23% more expensive than a year ago. Demand is strong and supplies are expected to tighten which is supportive to price.

Brent crude petroleum price (May 22nd): $ 35.13/barrel Brent had gained on optimism about a potential COVID-19 vaccine, the easing of pandemic-related restrictions plus hope of a resulting demand recovery and dropping crude oil production and stocks. Recently it lost a bit on doubts about how fast economies would recover, after the U.S. and China clashed over the imposition of a new national security legislation on Hong Kong. Some also worry about China's economic future after the National People's Congress, for the first time, didn’t set a specific target for economic growth this year. But as movement restrictions around the world ease, demand will of course pick up. Still, petroleum prices are way down compared to vegetable oils, making biodiesel uncompetitive/unattractive (where not mandated).

Source: Trading Economics

1 EURO (May 22nd) = USD 1.0904 The Euro depreciated on Friday on concerns over the Eurozone’s economic recovery and as demand for the USD increased due to rising political tensions between the U.S. and China.

Source: ECB

We are here to help. Meanwhile, take good care of yourself and each other.

Don't forget to check out our other bi-weekly updates!There is some complexity to the business we daily operate in. To help understand the business of being an edible oil and fat producer we've launched this bi-weekly newsletter. Sign-up for Aveno's newsletters!

DisclaimerUnless otherwise mentioned the crude oil values quoted in these documents are prices landed in EU without import duties, handling, storage, financing, refining, packing, transport or any other cost related to bring the product to market. They are used as market trend illustration. Substitution of oils is possible but different oils have different fatty acid profiles and are not all interchangeable for all applications. One can make biodiesel from all oils and fats but one cannot make mayonnaise from coconut oil. This document is exclusively for you and does not carry any right of publication or disclosure. This document or any of its contents may not be distributed, reproduced, or used for any other purpose without the prior written consent of AVENO. The information reflects prevailing market conditions and our present judgement, which may be subject to change. It is based on public information and opinions which come from sources believed to be reliable; however, AVENO doesn’t guarantee the correctness or completeness. This document does not constitute an offer, invitation, or recommendation and may not be understood, as an advice. This document is one of a series of publications undertaken by AVENO and aims at informing broadly a targeted audience about the edible oils & fats market. AVENO’s goal is to keep this information timely and accurate however AVENO accepts no responsibility or liability whatsoever with regard to the given information.

Read in browser »

|