Fireworks for the New Year and fireworks in commodities!During and after our Christmas break many of us saw New Year's Eve Fireworks and fireworks in most commodities!

Your Bi-weekly update on edible oils & fats by Aveno

January 10th, 2020

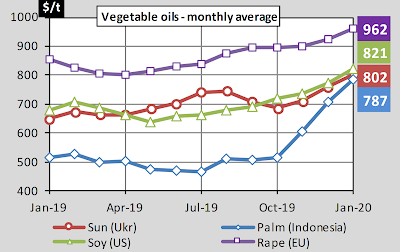

Market evolution in the past 4 weeks(running month + 3 = APRIL position, refined, in euro):

On Friday December 13th came the long-awaited announcement about “the phase 1 trade deal”, following the trade war that started in 2018. Optimism for the global economy made commodities and the stock exchange appreciate. Higher economic growth increases demand for commodities: more people with more purchasing power buy more stuff. Copper soared to its highest level in 7 years. Also, aluminum, nickel, zinc, petroleum and others followed and so did soft commodities. Around Christmas, in Kuala Lumpur, palm oil hit a 3 year high above 3000 Ringgit.

The “deal”, planned to be signed on January 15th (could fire up market again), so far only means there will be no further escalation of the trade war: no new tariffs; but removal of old tariffs is still far away. Markets might have overreacted. For agricultural products China was once the 2nd customer of the US and now ranks 5th as it has spread its supply chain risk over several suppliers around the globe. Some believe that any increase of production (of any supplying country) in anticipation of higher Chinese demand could result in an oversupply and collapse of prices.

source: Thompson Reuters

Economists teach us that free trade creates both winners and losers, but that the profits are greater than the losses. If profits compensate the losses, the country as a whole is better off. But this is based on the, often concealed, assumption that the country's trade balance is in surplus or balanced. If trade deficits accumulate year after year, the group of losers in that country grows bigger. The US has had trade deficits for over more than 40 years and there the group of losers has only grown. In November, the US trade deficit of $ 43.1 billion was at its lowest level in three years. That the US imports just all products from the rest of the world may soon be a thing of the past.

A new reality we’ll have to deal with and maybe we are witnessing the start of the end of globalization, accelerated by climate change policies such as Europe’s New “Green Deal”: carbon footprint of imports, Europe halting the use of palm oil for biodiesel, the EU Commission to tackle deforestation (South American soybeans and Indonesian palm oil). Or producing countries like Brazil and Indonesia promoting the use of biodiesel to reduce CO2 emissions. Higher prices for cleaner bunker fuels that fuel ship’s engines etc.

Source: European Commission / IGC, Monthly average close Jan. 9th

Lately a stronger dollar and concerns about the tensions in the Middle East weighed on the market and for example lauric oils chickened out for several tens of dollars/ton (volatility!). Amidst geopolitical uncertainties it is always wise to return to basics and look at some fundamentals: - Brazil to set record soybean crop, provided weather stays ok. Argentina: plantings in progress; export taxes disturb trade.

- Rapeseed shortage in EU will not go away and crude rapeseed oil already broke through the $900 marker! Weather/fire problems in Australia. + good biodiesel offtake.

- India, the biggest edible oil importer in the world, will keep importing, but remains to be seen how high prices can go before demand drops.

- Due to the ASF the Chinese produce less soybean oil and need to import more oils and fats.

- Lower palm oil production and stocks + biodiesel mandates.

- Less production of animal fats and more usage in biodiesel production.

- Sun market continues to trade a carry, with stock levels in the Black Sea relatively high. Relative price competitiveness of sunflower oil attracts other demand from food and biodiesel. Refining capacity already well sold till mid-2020. High Oleic sun premiums pressured.

Brent crude petroleum price: $ 65.34/barrelSource: Trading Economics Refueling becomes slightly more expensive due to an increase in the share of biofuels:The share of biofuels in diesel and gasoline increases slightly January 1st onwards. The price at the pump also rises slightly, with around 2 cents per liter. A European directive obliged the member states to increase the share of biofuel in diesel and gasoline to 8.5 %. In Belgium diesel and gasoline will even have to contain 9.6 % of biofuels. In addition, there is a second European directive, which obliges member states to reduce CO2 emissions from fuels by 6 % in 2020.

EURO (9 January 2020): EUR 1 = USD 1.111

Source: ECB

Optimistic investors left the traditional safe havens such as gold and the so-called safe currencies as the Yen and dollar which has been rising almost continuously, at a gradual pace, since 2018 against the Euro. The American economy remained strong in 2019 and any potential (global) economic slowdown or recession has been delayed by interest rate cuts. In 2020 economic growth may slow down, but most analysts do not expect a recession. In this election year, Trump will do everything not to slow down the economy and to bring down the value of the dollar. Trade balance and balance of payments have been negative for years and the US government deficit and debt continue to rise. Many observers think the dollar has peaked and that lesser times are coming for the US currency.

Don't forget to check out our other bi-weekly updates!There is some complexity to the business we daily operate in. To help understand the business of being an edible oil and fat producer we've launched this bi-weekly newsletter. Sign-up for Aveno's newsletters!

DisclaimerUnless otherwise mentioned the crude oil values quoted in these documents are prices landed in EU without import duties, handling, storage, financing, refining, packing, transport or any other cost related to bring the product to market. They are used as market trend illustration. Substitution of oils is possible but different oils have different fatty acid profiles and are not all interchangeable for all applications. One can make biodiesel from all oils and fats but one cannot make mayonnaise from coconut oil. This document is exclusively for you and does not carry any right of publication or disclosure. This document or any of its contents may not be distributed, reproduced, or used for any other purpose without the prior written consent of AVENO. The information reflects prevailing market conditions and our present judgement, which may be subject to change. It is based on public information and opinions which come from sources believed to be reliable; however, AVENO doesn’t guarantee the correctness or completeness. This document does not constitute an offer, invitation, or recommendation and may not be understood, as an advice. This document is one of a series of publications undertaken by AVENO and aims at informing broadly a targeted audience about the edible oils & fats market. AVENO’s goal is to keep this information timely and accurate however AVENO accepts no responsibility or liability whatsoever with regard to the given information.

Read in browser »

|