Thursday, Feb 8 - MAHC Member Meeting, 9-10:30 am, Maine Housing, 26 Edison Drive, Augusta

In person panel discussion on the Affordable Housing Investment Market. Hybrid meeting access. Email for remote link.

Jan 29, by 5 pm - Submit Testimony On Proposed DEP Rule Changes That Will Increase Lead Times and Carrying Costs for Affordable Housing Changes are proposed to Chapter 2 of DEP rules. Chapter 2 governs the processing of license applications, appeals of Commissioner license decisions to the Board, petitions and motions to modify, revoke or suspend licenses, petitions for corrective action orders, and other determinations on specific matters as described in the rule. This has a direct impact on the development of affordable housing. MAHC will submit testimony in opposition to the proposed changes. Sharing below an overview from Pierce Atwood on these changes:

"Although the DEP’s changes affect almost every provision in Chapter 2, a summary of which is linked here, the most notable changes the DEP proposes are:

Adjusting requirements for the BEP to take jurisdiction over a project application, including a new provision allowing the Commissioner to request that the BEP assume jurisdiction over an application at any point during the processing of that application. This will make it easier for project opponents to increase costs and delays by pushing the BEP to take jurisdiction over more projects.

Expanding the Department’s consideration of the threshold issue of Title, Right or Interest (TRI), including a burden shift to the applicant where TRI is challenged by opponents at any time during the application processing period, and a requirement that TRI be demonstrated across the life of the project (including through decommissioning).

Extending DEP processing times on various submissions including for scheduling pre-application meetings (now 60 days) and pre-submission meetings (now 45 days), as well as permit by rule decisions (now 20 working days for most permits by rule), among others.

Clarifying that a “Project” means all portions of an activity for which Department approval is required.

Expanding notice and public meeting requirements.

Changing BEP appeal procedures, including additional circumstances under which the BEP Chair may dismiss an appeal.

Clarifying that the BEP can modify a license while a judicial appeal is pending.

Adding a mechanism for voluntary recission of a permit.

Adding rules governing Administrative Consent Agreements, which will require BEP approval."

SUBMIT TESTIMONY: Bill Hinkel, 17 State House Station, Augusta, ME 04333-0017, 207-314-1458 Comment deadline: January 29, 5 PM

MAHC Testifies for Increase to State Historic Tax Credit - You Can Still Submit Written Testimony

Testimony in favor of LD2106 to the Taxation Committee to double the state historic tax credit from $5M to $10 million dollars to support affordable housing redevelopment. Testimony here. You can still submit written comment in favor here.This committee is new to housing issues and your voice matters. At the public hearing, there was good turn out and everyone spoke in favor of the bill. It will still need to have a work session with the Taxation Committee, and ideally move to Appropriations. Pictured below, LD2106 sponsor, Senator Peggy Rotundo, introducing her bill at the public hearing.

Good News: House Ways and Means Committee made a significant bipartisan move by approving the Tax Relief for American Families and Workers Act of 2024 that Expands Federal LIHTC Funding

The Tax Relief for American Families and Workers Act also includes provisions to support affordable housing. It increases the nine percent low-income housing tax credit ceiling by 12.5 percent for calendar years 2023 through 2025. Additionally, the act lowers the bond-financing threshold to 30 percent for projects financed by bonds issued before 2026. These measures aim to promote the availability of affordable housing options for individuals and families.

JOBS: Executive Director or Maine Redevelopment Land Bank, and Zoning Research Assistant Executive Director of Maine’s new Land Bank Authority. Job posting. Job description.

Part-time zoning research assistant to work with Backyard ADUs to research ADU and zoning laws across New England starting with the Portland, Maine area. PT flexible hours, work from home, 5-20 hours/week preferably about 10 hours/week. Preferred, but not required, college level work on land use. Possibility to evolve into full-time work. $20-25/hr. Please submit a resume, cover letter expressing your interest, and an example of written work by Feb 15 to: Liztriceconsulting@gmail.com

Housing Committee Schedule

Tuesday: 1/30/2024

1:00 PM PUBLIC HEARING

L.D. 2158 An Act to Improve the Housing Voucher System

1:15 PM WORK SESSION

L.D. 2136 An Act to Provide Financial Support for Shelters for Unhoused Individuals

L.D. 2138 Resolve, to Improve Funding for Homeless Shelters

L.D. 337 An Act to Amend the Regulations of Manufactured Housing to Increase Affordable Housing

L.D. 853 RESOLUTION, Proposing an Amendment to the Constitution of Maine to Establish a Right to Housing

Friday: 2/2/2024

9:00 AM Presentation – MSHA – Homeownership Program update

9:30 AM WORK SESSION

L.D. 2158 An Act to Improve the Housing Voucher System

L.D. 772 An Act to Establish a Process to Vest Rights for Land Use Permit Applicants

L.D. 1752 Resolve, to Prepare Preapproved Building Types

Discussion of HOU bills on the Appropriation’s table

SIX TAKEAWAYS FROM AMERICA’S RENTAL HOUSING 2024

JCHS new report America’s Rental Housing 2024, examines the state of rental housing in the US, including the critical affordability and policy challenges facing the nation. Among the report’s many takeaways, six key findings stand out.

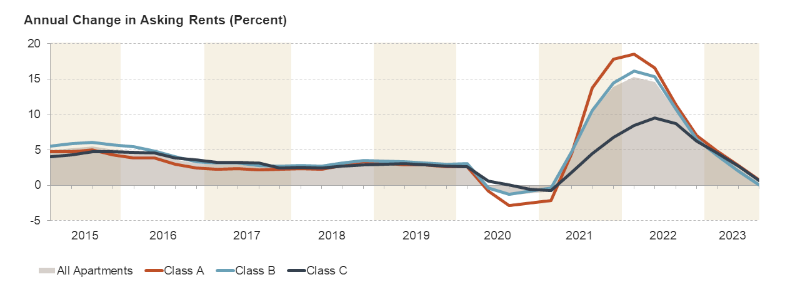

1. Rental markets are softening. After an overheated 2021 and 2022, rental markets finally showed signs of cooling. Apartment rent growth peaked at a record-breaking 15 percent annually in the first quarter of 2022 before starting to decelerate (Figure 1). By the third quarter of 2023, rents grew by just 0.4 percent year over year.

Figure 1: Apartment Rent Growth Has Stalled

Notes: Asking rents are for professionally managed apartments in buildings with five or more units. Class A (Class C) apartments are relatively higher (lower) quality. Source: RealPage.

Rising vacancy rates helped slow rent growth. The apartment vacancy rate climbed to 5.5 percent in the third quarter of 2023 from a record low of just 2.5 percent in early 2022. Historically strong multifamily completions were primarily responsible for pushing up vacancy rates; 436,000 multifamily units came online in the third quarter of 2023 on a seasonally adjusted annualized basis.

2. Affordability is worse than ever before.

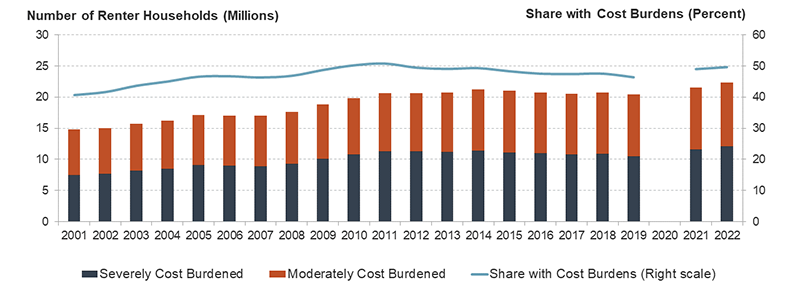

Although rental markets are cooling, asking rents remain above pre-pandemic levels and affordability conditions are the worst on record. In 2022, the number of cost-burdened renter households hit a new high of 22.4 million (Figure 2). This marked an increase of 2 million households since 2019 and pushed up the share of cost-burdened renter households to 50 percent, a 3.5 percentage point jump in just three years.

Figure 2: The Number of Cost Burdened Renters Hit an All-Time High

Figure 3: US Continues to Lose Low-Cost Rental Housing

3. Housing instability is rising.

Early pandemic efforts to keep renters housed—including eviction moratoriums, income supports, and a $46.55 billion emergency rental assistance program—were winding down as rents skyrocketed, leaving many renter households vulnerable to housing instability. At the end of 2022, evictions neared pre-pandemic levels and remained elevated through the middle of 2023, when about 12 percent of renter households reported that they were still behind on rent.

The end of pandemic relief measures and historically high rent growth also led to a dramatic rise in homelessness. The number of people experiencing homelessness jumped by nearly 71,000, from January 2022 to January 2023, the largest single-year increase on record, to an all-time high of 653,100 people.

4. Rental assistance falls far short of the need.

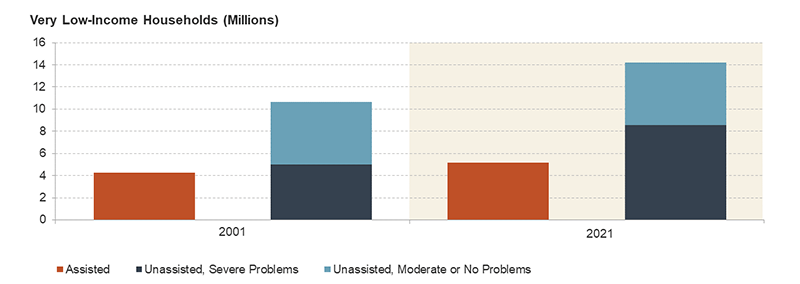

Despite deteriorating housing affordability and stability, rental assistance has not expanded to meet the growing need. The number of very low-income renter households making no more than 50 percent of area median income grew by 4.4 million from 2001 to 2021, but the number of assisted households in this income range increased by just 910,000. This left 14 million income-eligible households to fend for themselves in an increasingly unaffordable market (Figure 5). Of those not receiving assistance, 8.5 million experienced worst case housing needs, meaning they spent more than half of their income on housing and/or lived in severely inadequate housing. A full 60 percent of unassisted households had worst case needs in 2021, up from 47 percent in 2001.

Figure 5: The Rental Assistance Shortage Continues to Worsen

5. The rental stock has significant investment needs.

The rental stock is older than it has ever been with a median age of 44 years, up from 34 years two decades ago, and heightening the need for substantial investments. As of 2021, nearly 4 million renter households live in substandard conditions and even many physically adequate units have significant repair needs. The Federal Reserve Bank of Philadelphia estimated it would cost $51.5 billion to address the repair needs of the occupied rental stock.

The rental stock also requires upgrades to reduce its contribution to climate change and improve its resiliency to environmental hazards. About half of renters making less than $30,000 experienced energy insecurity in 2020, and extreme weather variability and rising temperatures will only increase home energy demand and renters’ housing costs. The Inflation Reduction Act included about $9 billion for household rebates and tax credits for approved upgrades as well as $1 billion to make the HUD-assisted stock more energy and water efficient. Additional federal resources are also needed to make resiliency improvements for the 18 million occupied rental units in areas with at least moderate annual economic losses from environmental hazards (Figure 6).

6. High interest rates are dampening rental market activity.

The high interest rate environment over the last year has increased the cost of debt to acquire and build multifamily properties. High treasury yields have also pushed up the cost of equity as apartment investors expect greater returns to compete with relatively low-risk treasuries. In this environment, deals are less profitable, which has depressed both multifamily lending and apartment transactions.

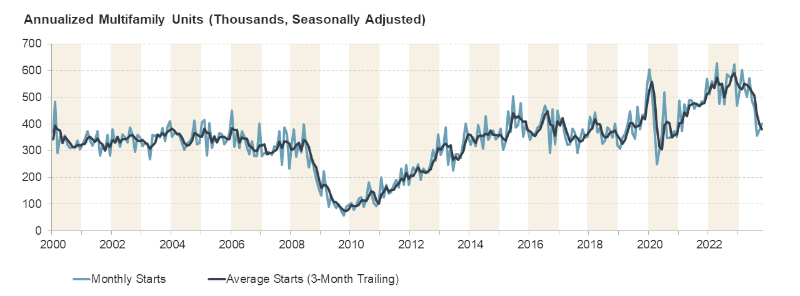

Most concerning is the swift slowdown in multifamily construction. Though starts climbed during the pandemic and remained among some of the highest levels in the last two decades through the first half of 2023, hitting a seasonally adjusted annual rate of 571,000 units in May, they have since dropped. By October, starts were down 30 percent year over year (Figure 7). While there are a record-high number of units currently under construction, continued market cooling and high interest rates could lead to further declines in multifamily starts, creating supply challenges down the road.

Figure 7: New Multifamily Construction Has Quickly Declined

MAHC Testifies in Favor of LD337 to Allow Manufactured Housing in All Single Family Zones - Testimony Here

JCHS Data to Support this Policy: FIVE BARRIERS TO GREATER USE OF MANUFACTURED HOUSING FOR ENTRY-LEVEL HOMEOWNERSHIP

The sharp rise in home prices and interest rates over the last few years has pushed homeownership out of reach for millions of renters, as documented in our State of the Nation’s Housing 2023 report. Under these conditions, it is more important than ever that affordable homes are available for entry-level homeownership. Manufactured housing offers just that, thanks to lower production costs; indeed, the construction cost of a basic single-section manufactured home is roughly 35 percent that of a comparable site-built home. While the savings for larger homes is smaller, it is still significant, with a double-section home costing 60 percent, and a CrossModTM home (which most closely resembles site-built housing) costing 73 percent of comparable site-built homes.

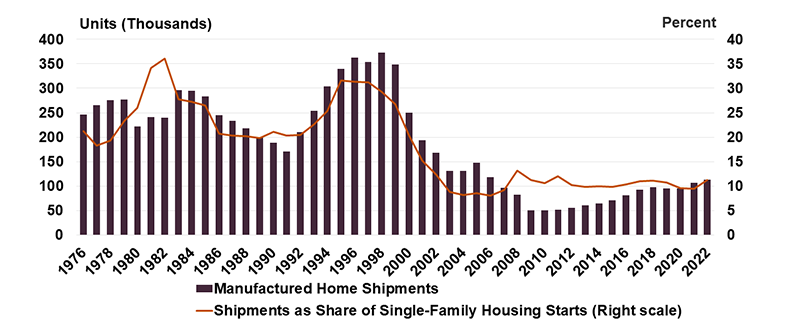

Despite these savings, manufactured housing production remains depressed. During the 1980s and 1990s, more than 250,000 homes were produced on average each year, amounting to 25 percent of the volume of single-family construction (Figure 1). In recent years manufactured home production has just topped 100,000 units annually, about 10 percent of the volume of new single-family homes.

Figure 1: Manufactured Home Shipments Since 1976

Given the cost advantages and unmet need for more entry-level housing, why has production of these homes remained so low? In our new paper, “A Review of Barriers to Greater Use of Manufactured Housing for Entry-Level Homeownership,” my co-authors and I synthesize what is known about the limiting factors to help identify steps that could increase the production of this important form of housing. Specifically, in our review, we discuss five key barriers:

Negative Perceptions of Manufactured Home Quality

Restrictive Zoning and Land Use Regulation

Market Conditions

A Unique and Limited Supply Chain

Access to Mortgage Financing

SAVE THE DATE: MAHC Housing Conference – Nov 13

This all day conference held every other year delves into housing and policy issues impacting addressing the need for housing in Maine and nationally. Hear from business and municipal leaders working on housing, statewide elected officials, housing policy leaders, development professionals and more. Attend to network with who’s who in Maine’s housing development world and understand the opportunities and challenges we face in the policy realm to meet Maine’s need of 80,000 new homes by 2030. With a presidential election, and a new Maine legislature starting, this is the event to understand what’s ahead for housing and how to get involved in advocacy so all Maine people have a home.